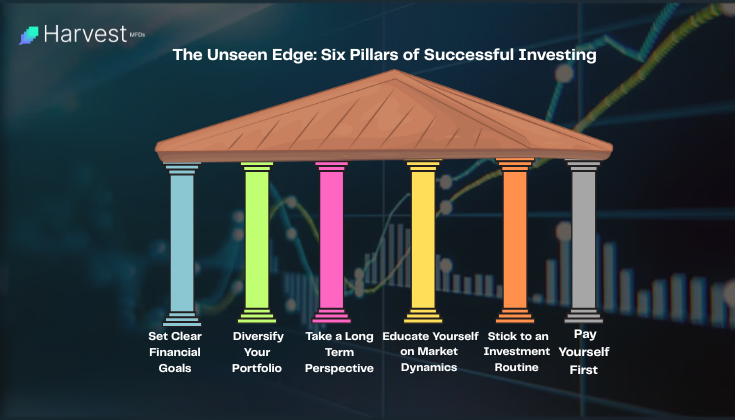

Pursuing trending stocks or having perfect market timing are not the keys to successful investment. It all comes down to developing the proper attitude and reliable routines. These thought patterns and actions ultimately decide whether you create enduring riches or see your earnings disappear in panic attacks. Let's examine six essential attitudes and actions that form the foundation of any successful investor's strategy.

Decide where you want to go before you even create a brokerage account. Without a map, you can drive across the nation and wind up somewhere you didn't plan to go. Investing is no different. Clearly state your objectives in quantifiable terms.

Are you saving for a down payment on a house in five years or for a pleasant retirement at sixty? Establish a realistic timeframe and an exact monetary amount. Divide your goal of having Rs500, 000 retirement fund in 20 years into monthly and annual savings goals. This turns intangible goals into tangible actions.

Review these objectives on a regular basis, at least once a year, to take into consideration adjustments for changes in income, expenses, or personal circumstances. Use a portion of any bonuses you receive to further your objectives. If unforeseen medical expenses occur, make the necessary adjustments and recalculate without compromising your main strategy.

Goals that are clearly specified have several uses. They help you narrow your investment approach, enabling you to allocate conservatively for short-term requirements and aggressively for long-term objectives. They offer a benchmark for gauging advancement. Additionally, having specific goals helps you remember why you started, which prevents you from panic selling when the market declines.

The saying, "don't put all your eggs in one basket" is surely familiar to you. That's precisely what investing diversity entails. Your entire portfolio is at risk if you invest all of your money in one kind of investment, such as tech stocks, and they all plummet. However, if you distribute your funds among other investment types that move differently, the loss of one won't destroy the others.

Stocks, bonds, and possibly even commodities or real estate are all part of a well-diversified portfolio. These assets respond to changes in the market in different ways. For instance, in a thriving economy, tech stocks may rise, but bonds often remain stable when the economy slows down. They balance each other out since they are not directly connected; if one falls, the other may hold or rise. Using mutual funds is a simple approach to diversify. One fund can provide you with a variety of assets, such as stocks from numerous nations or hundreds of different bonds, rather than requiring you to choose numerous separate investments.

Short-term stock market fluctuations are common; one week they may be up, the next down. Markets, however, have a tendency to increase over time if you zoom out and consider the wider picture. Consider Pakistan's KSE-100 Index, which has increased from a few hundred points in the early 1990s to over 118,000 points presently (and much higher recently) over the last 20 to 30 years. That is a blatant indication that long-term investors have made money.

What causes this to occur? Businesses generate profits as economies expand, and when you reinvest those earnings (such as dividends), your investment continues to grow because of a phenomenon known as compounding. As a basic illustration, if you invest Rs 10,000 with an annual return of 8%, you will have almost Rs 20,000 in ten years, Rs 46,000 in twenty, and almost Rs 100,000 in thirty years, all without making any additional investments. That's what patience and letting your money develop naturally are all about. Thinking long-term also helps in difficult circumstances. Many people panic and sell when the market declines, such as during a financial crisis or periods of political unrest. However, history demonstrates that those that remain composed or even increase their investments during downturns end up winning. Holding on provides you a chance to recoup, but selling out of fear locks in your losses.

Your level of knowledge is one of the few factors in investing that you can control. You will make fewer mistakes the more you learn. Spending 15 to 30 minutes a day reading financial news can train your brain for wise investing, much like going to the gym helps you grow your physique. Start by explaining basic concepts like inflation, the actions of the Federal Reserve or State Bank, or the revenue streams of large corporations. Knowing how these factors impact the market allows you to predict potential future developments. Try to understand the fundamental instruments used by investors to evaluate stocks. For instance, dividend yield indicates the return you're receiving, free cash flow indicates how much actual money a company is creating, and the price-to-earnings ratio, or P/E ratio, helps you determine whether a stock is too expensive. These factors aid in your decision to wait or purchase. Recognize how your own brain can deceive you as well. Sometimes we copy others without question (herd mentality) or we just seek out facts that supports our beliefs (confirmation bias). These are typical errors. Create a quick checklist to serve as a reminder: "Am I following a crowd? Am I overlooking warning signs? That way, you stay clear-headed.

Real money is not required to begin studying. To test your ideas using fictitious money, use free applications or paper trading platforms. This is something that many internet brokers provide. It's a secure method to hone your abilities prior to making actual investments. In short, the more you educate yourself, the more you’ll stand apart from people who blindly follow hype on social media. Smart investors keep learning, stay calm, and make their own decisions based on facts — not emotions.

Periodic outbursts of hyperactivity are defeated by consistency. Discipline is ingrained by an automated investment routine, which guarantees consistent contributions, astute oversight, and methodical rebalancing. For example, rupee-cost averaging entails investing a set sum (for example, Rs500) on a regular basis, independent of market conditions. By doing this, purchase prices are gradually smoothed out, eliminating the anxiety associated with attempting to "buy the dip."

Monthly automated transfers from checking to your brokerage, distributed based on goal percentages, may be part of your routine. Review performance every three months, and if allocations deviate greatly, make small rebalancing adjustments. Perform a more thorough audit once a year, taking into account tax-loss harvesting, comparing expense ratios, and assessing potential new markets. To keep track of what worked, what didn't, and the feelings that influenced decisions, record every move in an investing journal.

Automating investment duties removes uncertainty and lessens the desire to follow trends or "hot new strategies." Instead, you make steady progress toward your objectives under the direction of evidence and established guidelines rather than impulsive decisions.

Making saving and investing your first priority, just like paying your rent, is the most effective habit you can form. Set aside a specific portion of each paycheck (often 10–20%) to go straight into your investment accounts before distributing money for discretionary expenses. You won't be able to waste those dollars carelessly if you automate this transfer. "Out of sight, out of mind" gradually teaches you to live within your means while also increasing your portfolio.

Keep a sizeable emergency fund in a liquid, easily accessible vehicle, such as a high-yield savings account. Typically, this fund should cover three to six months' worth of living expenses. By keeping you from using long-term investments to cover unforeseen costs, this buffer protects your money and peace of mind.

"Paying yourself first" psychologically changes your identity from one of a consumer who saves leftovers to one of a saver who spends what is left over. You will receive positive reinforcement as your savings build, which will encourage you to keep up or raise your donations. These small contributions add up to significant wealth over years and decades when paired with market returns, which is evidence of careful saving and investing.

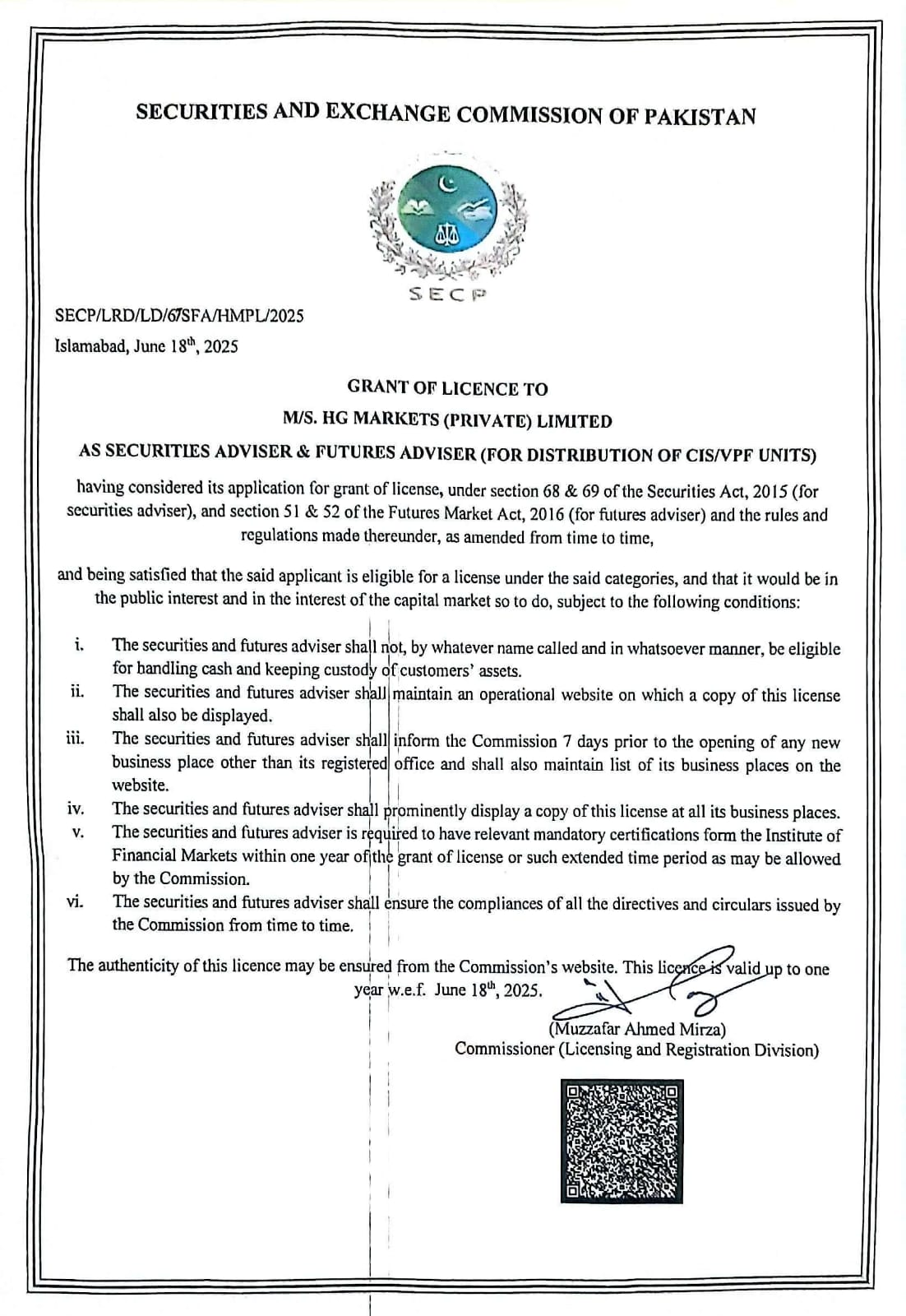

Harvest MFDs is a subsidiary of HG Markets. HG Markets is a TREC holder and broker of both the Pakistan Stock Exchange (MEM 528) and the Pakistan Mercantile Exchange (MEM 293). Licensed and regulated by the Securities and Exchange Commission of Pakistan (SECP), HG Markets holds the Securities Broker Registration Certificate (528/Securities Broker/2024) and the Futures Broker Registration Certificate (BRC 286)

.png)